2023: Writing More

I setup this blog a few years ago with the idea of writing regularly. Unfortunately, life, as it often does, got in the way. Over the last four years, I have moved country, started a new job focused more on the Macro side of investing and have bought a house. This combined with what I considered irrational markets meant that overall, I had little time to write about companies and markets in general. Now, as my personal situation evolves and the markets have sold off, I have started refocusing on investing, particularly in the Microcap space.

Why do I write?

Firstly, let me start off with saying that nothing on this blog is intended as advice. I will never tell you to buy or sell anything.

With that out of the way, the key reasons I write:

1) It helps shape my thinking and reasoning. If I can’t explain why I am invested in a company succinctly and clearly then I probably shouldn’t be there. Also, in forcing myself to write up a company, I quite often discover something else I should be looking at / considering.

2) I believe I write differently than a lot of buyside / investment commentators in Australia / New Zealand. There are a few things I can’t stand. Firstly, I hate stock pumping. A lot of people write up companies with little context. Any decent piece of research should also provide some information on risk and / or portfolio context. In addition, people should write about investments which go wrong and examine mistakes but very few people do and instead focus on rocket emojis. Secondly, there is something about being an investor or a fund manager that seems to make people think they are an expert on everything. For a few months last year, every fund manager was an expert on the Ukraine / Russia war (particularly those holding Russian stocks). Later in the year, we were subject to a number saying the only reason they were losing money was because of the Federal Reserve. Of course, they would also go on to say the Fed was wrong and they knew better than them. Again, discussions like this need to provide context. The reason you lost money is that you were positioned for zero rates continuing into perpetuity and you didn’t understand the risk.

So, with that in mind, context is going to be something I focus on here. I have started tracking a portfolio. It is a highly concentrated portfolio consisting of 6 micro caps and a bit of cash. It is highly concentrated because it is a small part of my family’s net worth and is (hopefully) the Alpha engine which sits alongside the house, super and cash. It is all in Australian and New Zealand microcaps currently because that is where I have been finding opportunities but there will be constraints to where I look. I will provide monthly updates as we go and at some stage will probably write a piece on holistic wealth management.

Whilst I am finding opportunities, this is in no way a call for the bottom of the market. To be honest, I have no idea where the overall market is going to go. I do believe the odds of a recession this year in the developed world are significant, I believe Tech (particularly the unprofitable and barely profitable) has further to fall, I believe more frauds will come to light and the less said about Crypto, the better… However, this is all healthy. We are getting back to a world where valuations matter and things make sense.

So to start the year, here’s a stock pump…

MHM Automation (MHM.NZ)

I wrote about MHM back in April last year.

In short, it was a basically a shell company with a long history that had a recapitalisation and made two small acquisitions that were working out well. In addition, it was looking to be a consolidator in the Food automation technology space.

Since I wrote about it, two significant things have happened. Firstly, they provided a very strong first half update (that’s good), and secondly, they announced a significant acquisition of a company called Wyma (could be good, could be bad).

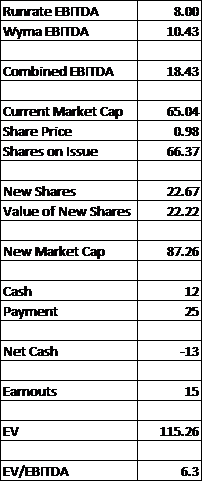

The uncertainty on the acquisition comes down to its size and lack of information. Based on the first half, MHM has an EBITDA runrate of c. $8m (purely from doubling the bottom end of the first half update), based on the acquisition multiple given, Wyma’s EBITDA is c. $10m. This is company changing. In terms of financial information, all we have is that one number on Wyma. If we fully dilute the capital base for the new shares, the cash payment (which pushes the company into debt) and the future potential earnouts, we get EV/EBITDA of 6.3x.

On that basis, it does look cheap and now is starting to look like a better scale business. However, without detail on Wyma it is hard to get carried away. I still hold the stock, I bought a small position in April last year and bought some more on the recent market update. That additional purchase plus the stock move has made it the second largest position in the concentrated microcap portfolio. In continuing to hold here, I am backing two things:

1) Management – they have executed the previous two acquisitions well. This is a bigger one but at least there is a track record there. Noting the current management has been in place since 2016.

2) The growth in the industry. MHM has been growing revenues strongly and is well positioned coming out of Covid. We need more information on Wyma, however we do have information on a peer, Scott Technology (SCT.NZ). Scott Technology has products in the Meat automation sector and that part of their business is fuelling their growth (chart below).

Source: Company filings

I have done some work on Scott Technology, and I wasn’t convinced. Partly due to the other divisions and partly due to the constant restating of their accounts. It’s not for me at this stage but I will keep an eye on it.

For now, I’m happy to hold MHM. It was always meant to be a rollup strategy, however the size of the acquisition has surprised me. I will be looking forward to seeing more information on it. Also, I have to note that it is subject to shareholder approval, finance and final due diligence so it is not a done deal yet. Targeted completion is 1 April 2023 so we should be receiving some more information in the not-too-distant future.