Adding some Growth

AI-Media Technologies (ASX:AIM) and RAS Technology Holdings(ASX:RTH)

Most investors describe themselves as either “value” or “growth”, or one of the many shades in between. I would describe myself as style agnostic, and to be honest the way I view it, the two styles are just different sides of the same coin (unless we are talking about true Deep Value which is a different story). Either way, everyone is trying to find an investment trading below the value of its future cashflows.

The reason for bringing up style is that last month I bought more in two of the more growth orientated positions in the portfolio. Both positions had sold off and potentially offered favourable entry points. Interestingly both businesses listed on the ASX at a similar time (4-5 years ago), and both are trading below their IPO prices. Both are around breakeven with regards to cashflow and profit and have trends that could potentially make them profitable over the next few years, meaning they are crucial inflection points in their corporate life. Both have net cash balance sheets and appear to need no further funding.

Please note that the below is just a summarisation of my thoughts and is in no way a stock pump. There will be no rocket emojis. In fact, with reporting season approaching, there is a chance I look very stupid in just over a month’s time.

The first position I bought more in is AI-Media Technologies (ASX:AIM). Ai-Media is a global provider of captioning technology. It is founder led, established in 2003 and listed on the ASX in 2020. The company made a major acquisition in 2021 of US company EEG Enterprises. It is through this acquisition that the company accelerated its trend from a human led captioning business to an automatic captioning business.

The key to AI-Media is the infrastructure of its captioning network, and not necessary the automatic captioning software itself.

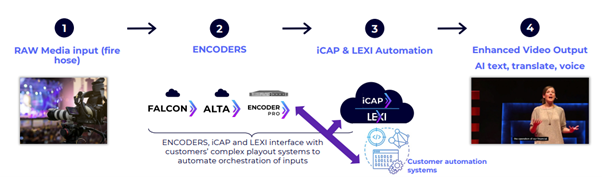

Source: Company filings

Customers buy an encoder, either a physical one, or a virtual/cloud one (Alta and Falcon in the diagram above). Those devices then connect to the iCap network which is the key asset acquired in the EEG acquisition. The iCap network then connects the customer with the most appropriate captioning solution, and this could be Ai-Media’s internal Lexi solution, which is automated, or a human captioner. The iCap network then uses its own capabilities to understand the context of what is being shown and automate / correct common words. The key asset therefore becomes the encoder and the iCap network, not necessarily the automated captioning software. There are multiple competitors in the captaining space, but they don’t have this same infrastructure.

I am a bit late to the party with this company. It has been well promoted, and it already has quite a few institutional shareholders on board. There are some institutions on board I would describe as good shareholders, and some that I would describe as not-so-good shareholders. I first started looking at the company below 40 cents and then it proceeded to double before I did anything. I bought a small position at higher prices and then bought a bit more this last month as it fell to the low 50 cent range.

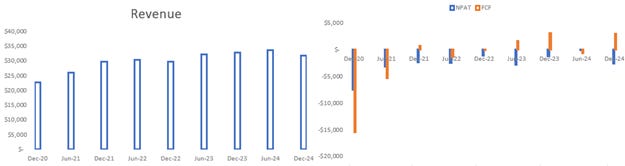

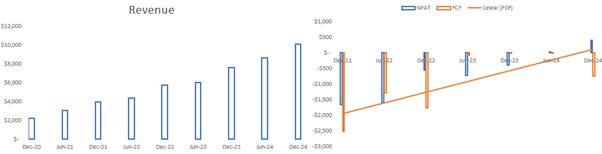

When you look at the overall financials, the growth doesn’t look very impressive. In totality there has been slight revenue growth, and the company is close to breakeven.

Source: Company filings, author’s calculations

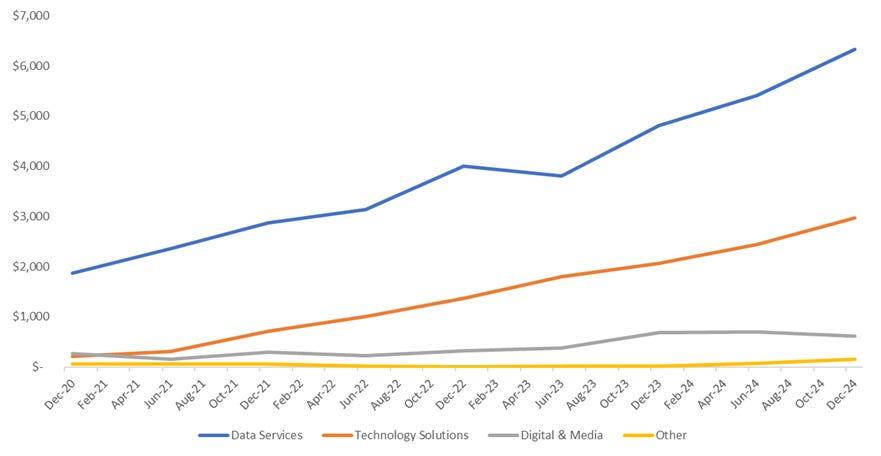

The reason for the sluggish revenue growth is that the company is effectively “eating its own lunch” by replacing low margin service revenue from human led captioning with high margin technology revenue.

Source: Company filings

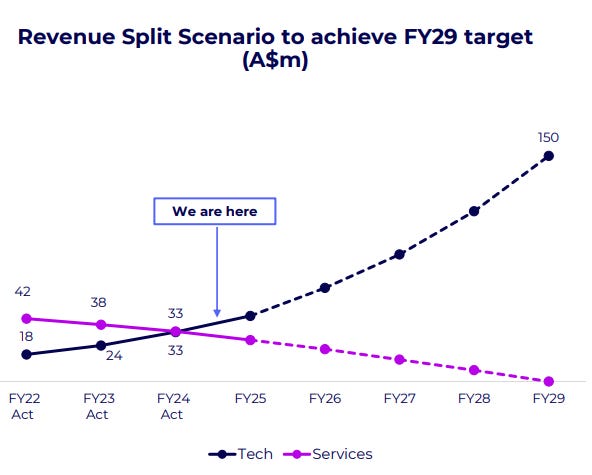

Hopefully, we are at a point as the above graph suggests where the growth in the technology revenue starts to drive the headline higher. A key driver of this growth is expected to be jurisdictional, with the company expanding in other markets outside of the US.

Source: Company filings

There is a lot more to this business than appears at first glance. The most recent results call saw the founder and CEO, Tony Abrahams, talk extensively about new products including Lexi Voice which provides real time voice translation. Tony can come off as overly promotional at times, but he has put his money where his mouth is and purchased shares fairly aggressively on market over the last few years.

The other position I bought more in was RAS Technology Holdings (ASX:RTH). It is a fairly new position for us, having bought it in April and written about it most recently in May:

Similar to AI-Media, the company is around breakeven when it comes to profit and cashflow, however with RAS, the revenue growth has been more consistent.

Source: Company filings, author’s calculations

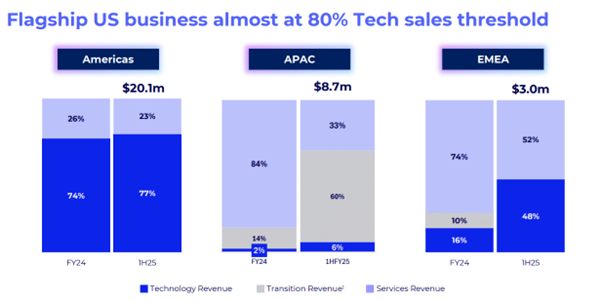

That revenue growth has come from two sources, Data Services and Technology Solutions.

Source: Company filings, author’s calculations

Data Services is the historic engine of the business. Through their platform they provide detailed data on racehorses to racing industry customers. They have a dominant market position in Australia with all the major betting companies signed up. Most impressively, they haven’t lost a customer in their 25 years of operation. A recent acquisition in Hong Kong shows intent to diversify geographically, and their UK business has been growing strongly albeit off a low base.

Technology Solutions is a relatively new field for them. This division takes their data services and incorporates it in an end-to-end wagering solution allowing customers to outsource their trading and risk management for horse racing. This can allow gambling / wagering operators in other sectors to enter a new market and leverage their existing client base.

The two positions above are not without risk. Both are near breakeven, so there is little valuation support, and they need to keep growing to justify the share price. We need to see operational leverage kick in once both companies are profitable, otherwise they can become capital traps. On the flipside, if that operational leverage does kick in, it can become a great thing. Once a company becomes consistently profitable, it gives investors something to value, and if they can continue to grow then the upside can be significant. It is at this inflection point where gains and losses will be made.

Just a friendly reminder that none of the above is investment advice, it is factual commentary on a portfolio run by the author.