August brought reporting season for a majority of our holdings and it didn’t go as smoothly as we would have liked. There weren’t any major disasters, however, across the board, almost every result could be described as “mixed”, with some positives and some negatives coming out of each of them. Probably the sole disappointment was Vitura Health (ASX:VIT) where growth stalled in the 2nd half of the financial year. The remainder of the holdings, all continued to show some positive signs.

With the mixed nature of the results, the portfolio fell 0.73%, a huge 1bp ahead of the All Ordinaries which was down 0.74%. Year to date, the portfolio is up 21.9% versus the All Ordinaries up 7.0%.

Moving on to the results.

SRG Global (ASX:SRG)

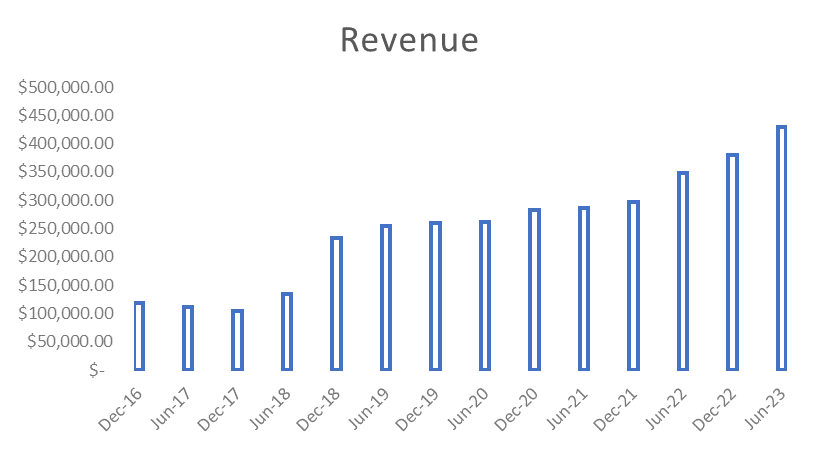

The result from SRG was solid, albeit a little bit messier than recent ones with some one-off expenses. Revenue growth was strong, with organic growth as well as the acquisition of the ALS Asset Care business boosting it. Overall, revenue was up 26%.

Source: Company Filings, Author’s Calculations

Earnings rose as well. EBITDA was up 40% and NPATA which excludes one-off costs was up 42%. The one-off were costs associated with the acquisition and the exit of the PT Business in Middle East and Australia. EBITDA growth ex the ALS acquisition was 31%.

Source: Company Filings, Author’s Calculations

The mess comes below those lines and reported NPAT fell. Free cash flow was also significantly weaker (negative in fact), with a working capital build for the first time in a while. That's not unexpected given the acquisition plus the growth in their work pipeline, which rose 46% over the year to $1.9bn.

Source: Company Filings, Author’s Calculations

Margins and returns both weaker on those one-offs and the balance sheet back to slight net debt on the acquisitions (although there is nothing major to worry about).

Source: Company Filings, Author’s Calculations

The outlook at first glance appears positive, with the company guiding to 20% EBITDA growth. However, it is important to note that next year will include a full year contribution from the ALS acquisition. The 20% growth equates to c. $16m in additional EBITDA. The acquisition on a full year basis will contribute an additional $10m based on the expectations at the time of acquisition (noting it contributed $5m this year). This means that that the organic growth is only around $6m or 7.5% on the current base. This growth rate seems low given the growth in the pipeline and the significant value of contracts announced over the last year.

Source: Company Filings

It is worth highlighting that the company guided to 25% EBITDA growth this year and the organic growth came in at 31% so there is a chance they are being conservative. In fact, in the years post digesting the SRG/GCS merger, management have tended to under promise and overdeliver. Even without overdelivering, the shares are trading on a low valuation at 10.6x NPATA on a historic basis and 8.8x on a forward basis. The company appears to be managing without experiencing much of a cost squeeze, which has been a significant concern, and whilst it will never trade at a high multiple, there is not a lot of growth (if any) factored into the share price.

SDI Limited (ASX:SDI)

SDI, much like SRG, reported strong revenue growth.

Source: Company Filings, Author’s Calculations

This growth was across all regions and a falling AUD helped as well.

Source: Company Filings

Gross profit rose as margins stabilised.

Source: Company Filings, Author’s Calculations

Although NPAT fell slightly.

Source: Company Filings, Author’s Calculations

There are a couple of drivers at play here. The main one was an increase in marketing and travel spend. Travel is back to pre-pandemic levels and the company is out attending exhibitions and marketing. It has had an impact of the top line, with an impressive 2nd half and hopefully those benefits continue into FY24.

Source: Company Filings

The 2nd driver was an increase in interest costs. The company took on debt to purchase a new site on which it will build a new facility.

Source: Company Filings, Author’s Calculations

The new site will enable some short-term growth through warehousing; however, the main benefits are longer term with relocation by FY27. This new site did not come cheaply ($60m vs current market cap of $101m) and is a huge bet on future growth.

Source: Company Filings

Markets are typically short-term focused so a FY27 completion date is unlikely to get them excited. There is also a question of funding and the company would most likely need a capital raising in order to complete the project.

Despite this, we continue to hold a small position. The shares aren’t overly expensive at 14.2x trailing and there was one really big positive in the result. To understand this positive, it’s important to understand the history of SDI. Bank in the 1990s, the company came to life by developing a silver-based Amalgam to be used in fillings instead of the traditional mercury-based Amalgam. Whilst Amalgam is still used in some cases, Aesthetic fillings have really taken over. In the latest result, we are seeing some really strong growth for SDI in the Aesthetic category. The R&D they have put into that space appears to be paying off.

Source: Company Filings

Just a friendly reminder that none of the above is investment advice, it is factual commentary on a portfolio run by the author.

To be continued in Part 2…