Please note: Prices / multiples are based on yesterdays closing price

In recent months, the Close the Loop (CLG.AX) share price has languished near its lows. Overall year to date it is down 18% and has been the biggest drag on our portfolio. When a stock falls, it is always a good idea to revisit your thesis around why you own it and whether that still holds. Recently, we have been doing just that, helped by some excellent presentations / interviews from management on Coffee Microcaps and Strawman. We have discussed the company several times on here in recent months, but here we wanted to go a little bit deeper.

A major risk with Close the Loop is that it has a limited track record. The company essentially came together via a merger and an IPO back in 2021. The two companies merging were Close the Loop and O F Packaging Group. Close the Loop was founded in 2001 and O F Packaging was founded in 1998, so there is a long operational history. Joe Foster, who was the founder of O F Packaging Group was selected to run the company as CEO and he retains an ownership stake of over 12%, which provides good alignment.

I have often referred to Close the Loop as a recycling business, but it is a bit more than that. The company itself refers to itself as being “a circular economy” company. The merger of the two companies above gave the company two main business streams. Firstly, Close the Loop specialised in the collection and recycling of toner and print cartridges. Secondly, OF Packaging specialised in the recycling of soft plastics. From the soft plastics, it could create more sustainable packaging products, rigid plastics and more recently its TonerPlas product which is an asphalt additive that makes roads last longer. In order to obtain goods to refurbish, clean or recycle the combined company now has 200,000 collection points in the US, 60,000 in Australia and 40,000 in Europe.

When it listed, the business was skewed towards the Plastic Packaging side. This has changed since and we will touch on why shortly.

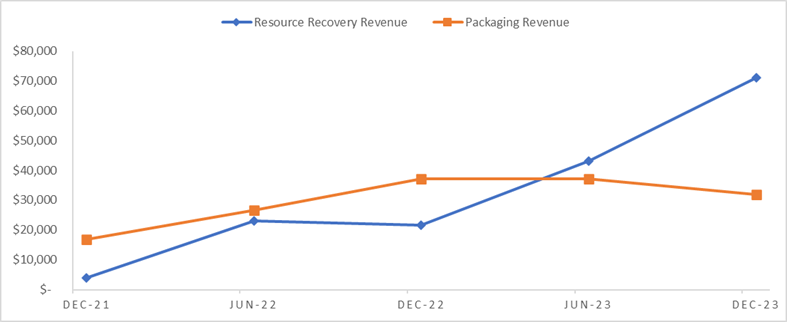

Source: Company filings

The early stages of its listed life saw growth across both divisions. However, in the last 12 months the packaging revenue has declined. This is the main negative in terms of financial performance we have seen from the company since listing, and it is fair to say that the performance of the share price would have been worse if not for acquisitions.

It is also possible that this is the main reason behind investors choosing to sell down the stock. Those who had invested at IPO would be disappointed with the initial business they invested in. The business has grown through acquisition, and in cases like this you can rightfully say that acquisitions are masking the organic decline.

However, we have come at Close the Loop from a different angle. We bought in after the acquisition of ISP Tek Services (ISP) in May 2023. When we look at the chart above, this acquisition is the primary reason for the rise in Resource Recovery revenue. At an EBITDA level, the shift is even more pronounced.

Source: Company filings

ISP is a US based electronics refurbisher which has a significant contract with HP. Essentially, US consumers have 30 days to return a product with no questions asked, if that happens with a HP computer or printer, it comes to Close the Loop, they refurbish it and it can be sold again. They then split the profit with HP.

Initially when Close the Loop acquired ISP, they operated on a one year rolling contract. Since acquisition, they have expanded that contract to 3 years, slightly derisking the massive concentration risk they have. That concentration risk remains but the term is expanded. One thing that could be a big boost for the company, would be acquiring another OEM (Original Equipment Manufacturer) as a customer. Currently, the other OEMs auction their goods off at discounted prices or refurbish in-house. This means the Close the Loop has little to no competition in this area (unlike the original Plastics and Printer Cartridge businesses), and if they can convince the other OEMs of the benefits of their model, there is significant upside.

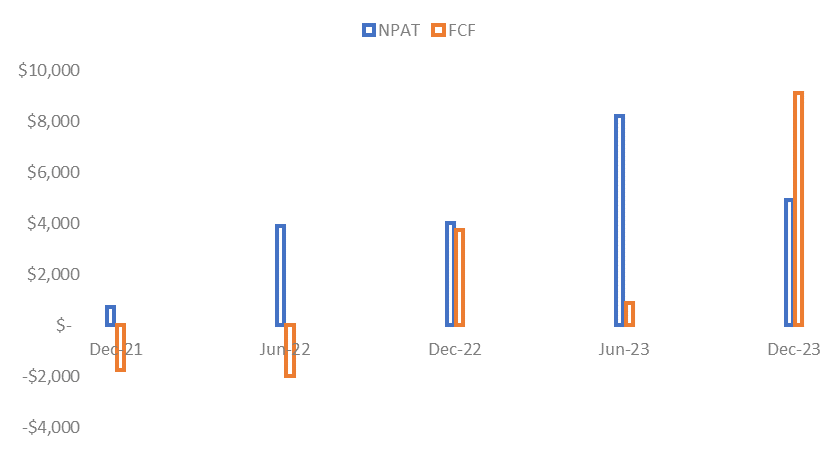

As seen above, the acquisition has seen revenue and EBITDA growth. Headline NPAT however has fallen.

Source: Company filings, author’s calculations

The company does report underlying NPAT, which strips out the amortization associated with recent acquisitions (NPATA), this came in at $13.3m versus the headline at $5m. Free cash flow was below the NPATA at $9.1m, so the company still needs to prove its cash conversion. Taking that FCF number as the lower of the two, the company trades on 9.2x the annualised rate from the last result (based on a share price of 31.5c).

The main negatives we have noted above are the lack of track record, the decline from the plastics division and the proof of cash conversion. Offsetting this are some positives, ISP appears to have been a very good acquisition and faces little to no competition. There is upside if they can win another OEM. There is also upside from their TonerPlas product on the plastics side, their first TonerPlas facility cost them $5m to build, is currently bringing in $4m in revenue and $1m in EBITDA. They plan to roll out multiple facilities across Australia and are seeking approval in other markets. Most of their facilities currently have capacity to increase production by the addition of additional shifts, so the company can grow with limited capex in the short term. In most cases, capacity can be doubled or tripled.

Growing businesses on low multiples are rare these days, as a relatively new listing with a large recent acquisition Close the Loop still has a lot to prove but for us the signs so far are good (albeit with weakness in one division). As a result of the recent share price weakness, we have continued to buy, and Close the Loop is now our largest position.

Just a friendly reminder that none of the above is investment advice, it is factual commentary on a portfolio run by the author.

This has been trashed now... Im a holder as well.

Any updates?

Mr Market has promptly responded to your write-up