May 2026 Update

Medium term growth? The market doesn’t care...

The post below contains mentions of Mayfield Group Holdings (ASX:MYG), Gentrack Group (NZX:GTK and ASX:GTK), Energy One (ASX:EOL), Aroa Biosurgery (ASX:ARX) and RAS Technology Holdings (ASX:RTH).

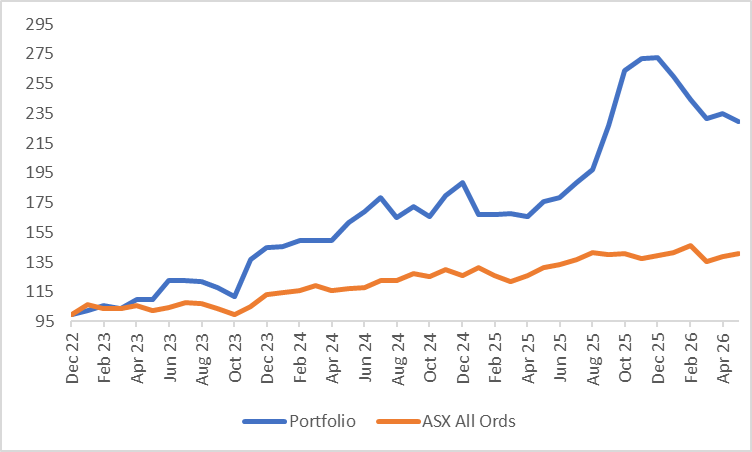

The portfolio was down 2.26% against a market that was up 1.22%. Liquidity and interest in micro-caps both appear to be low currently outside of certain themes and sectors, and that interest may stay low for the foreseeable future. That lack of interest does potentially create opportunities; however, one needs to be patient and also acknowledge when things have gone wrong. Since inception, the portfolio is up 129.9% well ahead of the All Ordinaries Accumulation which is up 40.4%.

For the month the best performers were:

Mayfield Group Holdings (ASX:MYG), +17.2%;

Scott Technology, (NZX:SCT), +12.7%; and

Aroa Biosurgery (ASX:ARX), +10.3%.

Mayfield announced $31m of new contracts including a single $15.7m contract to supply switchboards for a major data centre. The company has seen its work in hand grow from $1.04m to $151m over the course of this financial year.

Source: Company filings

It has also seen its share price rerate, going from $1.05 to $3.00 over that period. We maintain a small position and believe the next few years could see significant growth in revenue and profits; however, the price has clearly rallied on those expectations.

The other company with news in the list above was Aroa Biosurgery and we will discuss that below.

The worst performers were:

Gentrack Group (NZX:GTK and ASX:GTK), -39.1%;

Nova Eye Medical (ASX:EYE), -15.4%; and

Energy One (ASX:EOL), -12.3%.

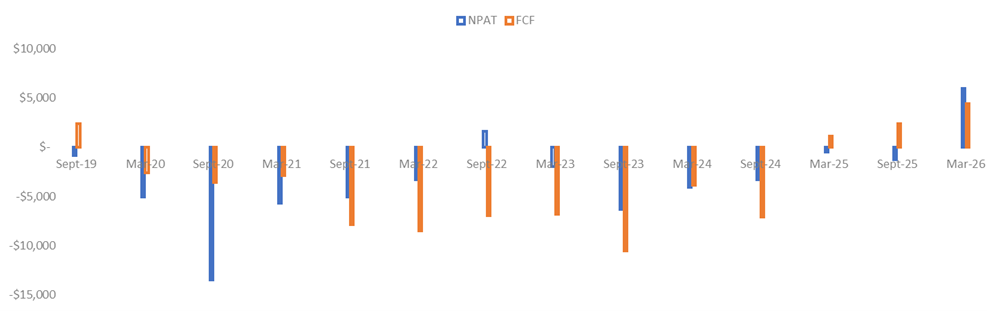

Gentrack and Energy One both downgraded expectations for this financial year. The Gentrack downgrade was the worse of the two. Their half year result saw revenue decline.

Source: Company filings, author’s calculations

This revenue decline came on the back of a fall in project revenue, and this was after the company had talked about 10 new potential large contracts six months ago. Over the last few years, the company’s cost base has grown as they invested in their g2 product, meaning that the fall in revenue was exacerbated in profits and cashflow.

Source: Company filings, author’s calculations

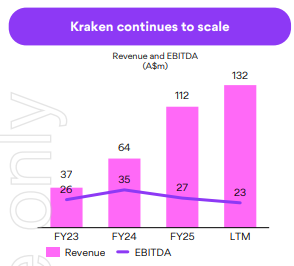

The company maintains the awarding of those 10 contracts have only been delayed and not cancelled. If that is the case, then FY27 could be a strong year. However, when you compare their recent history against Kraken (chart below), it appears that they may be losing the war.

Source: Origin Energy company filings

We had a small residual stake in Gentrack at the start of the month and sold that on the downgrade. We even wrote last month about our disappointment in the lack of news flow, that write-up can be found here:

Overall, our investment in Gentrack was successful with a majority of our position sold above NZ$10.

The Energy One downgrade was smaller in quantum, with Annual Recurring Revenue growing 13% over the year, slightly below the previous guidance of 15-20%. The company still continues to track well, albeit not as well as hoped.

To add insult to injury, Austco Healthcare (ASX:AHC) has announced a weak trading update on the first day of June. This all highlights the tough environment at the small end of the market currently. Bad news is being punished, and the reaction to good news can be muted if the benefits are not immediately visible in the short term.

This brings us to two positions that had positive announcements last month, Aroa Biosurgery (ASX:ARX) and RAS Technology Holdings (ASX:RTH). In both instances, the companies provided positive updates, but the responses were muted as other issues mean it will take a year or two before the bottom-line increases.

It reminds us of the below Simpsons scene, which is in turn a parody of The Fugitive. In this scene, Milhouse pleads his case to the FBI agent, who responds “I don’t care.” These companies are pleading to the market that they strong top line growth and solid medium-term prospects, but the market just doesn’t care.

Starting with Aroa Biosurgery (ASX:ARX), and they announced their full year result last month. The result was very strong. The 2nd half saw a big jump in revenue and EBITDA.

Source: Company filings, author’s calculations

And for the first time in its listed life, we saw a swing to profitability.

Source: Company filings, author’s calculations

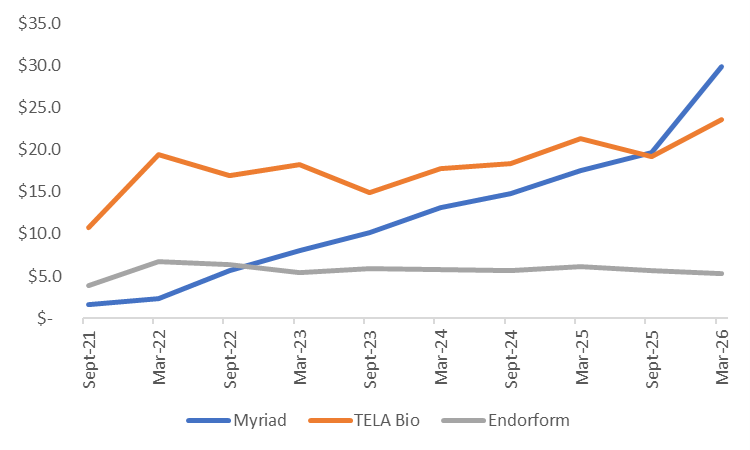

This growth story has been all about its Myriad range of products. Myriad is used in soft tissue reconstruction, and its growth is being driven by its use for large complex wounds and limb salvage. The performance of the product as well as its versatility means the financial outcomes for the hospitals using it are superior when compared to its competitors’ products. To continue the current momentum, the company is investing a further $5m in sales staff focused on Myriad.

Source: Company filings, author’s calculations

Myriad has now become their largest product, and importantly the company now generates 59% of its revenue via its own sales channels. Their Ovitex products, which are sold via TELA Bio have stagnated in recent years. TELA Bio has had contracting issues with hospitals in recent times; however, Aroa believe that these may be behind them. Despite that hope, they have guided for flat sales of Ovitex next year. A turnaround could provide some upside.

The main engine for growth in the medium term is not on that chart above, and that is their Symphony products. Symphony is used for complex chronic wounds, these being Diabetic foot and venous leg ulcers. Whilst this product has been approved for a number of years, the company has held back from selling it. The reason for this is that up until recently, high-cost products have been used because Surgeons received greater incentives from the suppliers. Aroa didn’t play this game and now this is set to change. The Center for Medicare and Medicaid Services has now stepped in and enforced a fixed price for these products. What was previously a US$10bn market is set to shrink and a number of competitors that relied on the higher prices are exiting the space (and are currently dumping product). The company has announced it will spend $4m on its sales capability for Symphony.

It is this $4m plus the $5m spend on Myriad above that is the main knock on the result. The guidance for next year is for 13-23% revenue growth, or direct revenue growth of 24-40% given that TELA Bio sales are expected to be flat, however EBITDA is expected to fall slightly. Ideally, we would like to see operational leverage flowing through, however the company believes investing for the medium term will provide a better outcome. If the company can continue to grow its Myriad revenue and replicate its Myriad success with Symphony, then that decision will be the correct one. Unfortunately, the market wants to see that success sooner.

Moving on to RAS Technology Holdings (ASX:RTH). RAS is similarly poised to Aroa, in that it is around breakeven but is yet to show the operational leverage that we hope for. Revenue is up; however, the company swung to a small loss in the last half.

Source: Company filings, author’s calculations

The bigger issue for RAS was the loss of the Stake contract, announced in December, and has rolled off at the end of May. Last month, the company announced additional contracts that will add $2m to Annualised Recurring Revenue (ARR), and this should more than offset the Stake loss. In addition to that $2m, the company has started to roll out its LeoVegas contract as of the first of May. The first part of the rollout is Sweden, with the bulk occurring in the first quarter of FY27. So, when we look at ARR, we should see a slight rise in the 2nd half of FY26 with a further rise locked in for the first half of FY27.

So, the company is still growing despite the Stake contract loss, and we therefore need to focus back on operational leverage. To that point, we wrote the following back in February:

“However, when we dig through, we become more confident than the headline results suggest we should be. The revenue and ARR growth were strong. The cost base has risen over the last year because of the Managed Trading Services (MTS) offering they have built. That spend is largely in place, they have built the team, and this allows them to bid for larger and higher margin contracts. The point around margins is crucial, any contract on their MTS offering and not outsourced comes in at significantly higher Gross Margins and is much more valuable to them.

From this position, winning a few contracts could tip them back into profitability and make the $37m market cap look very cheap.”

The full write-up can be found here:

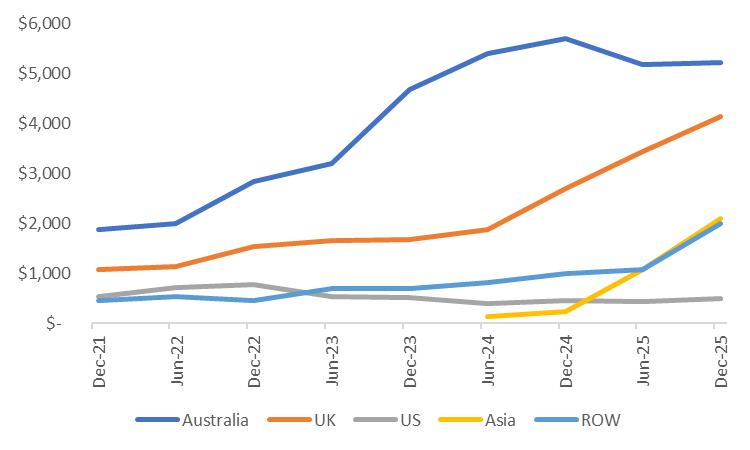

That $37m market cap has now become $30m and the market seems to have very little interest in the medium-term story. That story revolves around their MTS offering as well as geographical expansion. The key drivers of growth are the UK and Asia.

Source: Company filings, author’s calculations

Growth in both markets is expected to continue. The company entered Hong Kong in a meaningful way via an acquisition of publications in 2025 and in their recent announcement they highlighted strong momentum in the region. With Mainland China opening up soon, we would expect that to continue. Also, within that announcement they highlighted a contract win with Altenar in the UK, indicating gains in their other key market.

Both RAS and Aroa are at pivotal points, both are growing the topline but need to prove that their models are sustainable. The dynamic in the market has shifted away from rewarding companies with medium term ambitions and is very focused on short term cashflow. This potentially brings an opportunity. A fund manager I once followed had a concept of “time arbitrage”. Put simply, he used to believe that the market was predominantly short term (i.e. 1 year) focused, and that by focusing on a 2-3 year time frame, you could outperform. That fund shut down due to poor performance and outflows, so it didn’t work for him, but, hey, maybe it might work for us…

Just a friendly reminder that none of the above is investment advice, it is factual commentary on a portfolio run by the author.