December 2025 Update

Nothing lasts forever

The post below contains mentions of Symal Group (ASX:SYL), RAS Technology Holdings (ASX:RTH), Close the Loop (ASX:CLG), Energy One (ASX:EOL) Mayfield Group Holdings (ASX:MYG), and SRG Global (ASX:SRG).

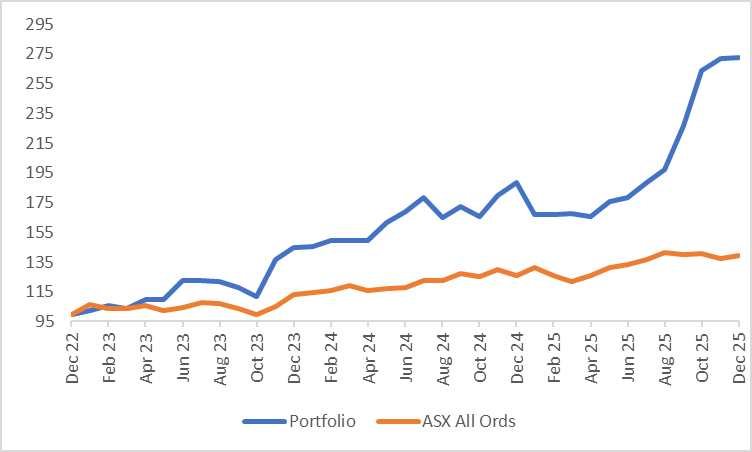

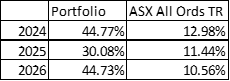

December brought to an end our 7-month streak of beating the market. The portfolio returned 0.17% against the All Ords Accumulation at 1.26%. In 2025, the portfolio returned 44.73%, well ahead of the All Ords Accumulation at 10.56%.

Over the three years we have been running this portfolio, we have seen strong returns albeit in a supportive equity environment. The broader market has provided low double digit returns whilst we have returned 44.77%, 30.08% and 44.73%.

We will look back at the last year shortly, however in the first instance we will review December. There were two companies that had an impact on the portfolio with announcements last month, one had a positive impact and the other had a negative impact.

The positive impact came from Symal Group (ASX:SYL), which finished the month up 25.3%. The company announced three bolt-on acquisitions. Firstly, they announced the acquisition of both Timms Group and L&D Contracting in Queensland. These are both civil contractors and cost an upfront amount of $28m with an earnout based on FY26 EBITDA. The expected EBITDA for these two businesses in FY26 is $8m. Secondly, they announced the acquisition of 80% of Davison Earthmovers in South Australia for $23.2m. Again, it is another business in the Civil construction industry, and this one is expected to generate $7m EBITDA.

There is a fairly clear strategy of rolling up businesses at 3-4x EBITDA, whilst themselves now trading above 6x. There is also a clear strategy to diversify nationally across Australia and across industries. We have had a good run with Symal with the shares up over 80% since we bought them in September. There is clear momentum which has been well assisted by institutional interest, with several fund managers having commented on it recently. Their earnings base is also increasing, their initial guidance for FY26 EBITDA provided at the FY25 results announcement was $115-125m. At the midpoint this reflected 13% growth. Since that guidance was issued, they have made four acquisitions, with a combined expected EBITDA of $18m. This suggests a current run-rate EBTIDA of $133-143m. The midpoint now reflects 25% growth. Due to the timing of acquisitions, some of this growth will fall into FY27.

The key question with any rollup is how long can they keep it going? It only takes one bad acquisition to bring down the whole thing. In a lot of cases, the best indicator of a company’s ability to grow via acquisition comes from its history. Symal has a very limited history as a listed company and hence, when we first bought the shares, they traded at what we considered a low multiple. However, they do have a longer track record of growth since being founded as a landscaping business in 2001. The founder still maintains a holding of 31% and a large part of the thesis is backing his ability to continue to execute.

When we first bought the shares in September, they were trading on a single digit P/E. After an 80% share rise, the valuation is no longer compelling. We continue to hold, but we aren’t in a rush to add.

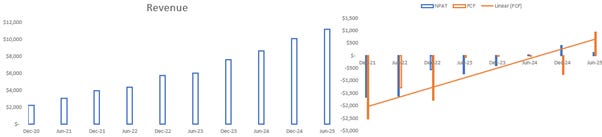

The negative announcement last month came from RAS Technology Holdings (ASX:RTH). RAS announced the loss of their Complete Racing Solution contract with Stake. This is particularly disappointing as the company can no longer say that they have not lost a tier one customer in their history. They lost this contract to ASX listed competitor, Betmakers, and that brings about questions around who has the superior product. Prior to this contract loss, the evidence has strongly been in RAS’s favour, however that is no longer the case.

If we step back and look at the bigger picture. This contract is likely seven figures in terms of revenue and will finish in May, meaning the impact is felt in FY27. For a company with at around breakeven and with only $21m revenue last financial year, this will be a significant hit.

Source: Company filings, author’s calculations

The good news is that RAS won a contract off Betmakers in the prior month. That contract was with LeoVegas group and will likely offset the Stake contract. Ultimately though, we are looking for the operational leverage to kick in and for the company to grow above breakeven. The two contracts offsetting means we are back to where we are started with regards to FY27, which is not ideal for a company that we were expecting to grow. We reduced our position slightly, however we still hold a decent position, albeit with less conviction than one month ago. It is particularly disappointing as we had been buying some after the previous contract win and were very excited about the year ahead.

Turning to the 2025 calendar year as a whole, it was a successful year for us overarll after a very rocky start. Our return of 44.73% came after we were down 11.25% in January. That fall in January was on the back of our position in Close the Loop (ASX:CLG). From the end of the year to our eventual sale, the position fell 57.4%. This was a 22.1% position for us and cost us c. 12.7%. Thankfully, we have recovered that and more since. It is also worth highlighting that the shares are down over 60% since our sale, so the decision to exit despite the heavy loss was vindicated.

We have written extensively about our mistake in Close the Loop, most recently in June:

In that write-up, we examined the disconnect between their earnings and their cashflow. It was something we had identified previously, but unfortunately, we ignored it.

Offsetting this fall in January were three stocks that rose by over 100% over the last 12 months, these were:

Mayfield Group Holdings (ASX:MYG), +290.6%;

Energy One Limited (ASX:EOL), +162.8%; and

SRG Global (ASX:SRG), +118.8%.

Energy One rallied on the back of both its half year result in February, and its full year result in August. We first wrote about Energy One in September last year:

I’ve posted that link because our thesis has largely played out as expected. At the time we wrote:

“As mentioned above, what we have seen to date with Energy One is revenue growth with some profit but little in the way of operating leverage. With this significant increase in sales staff, and the restructure mentioned above, we believe there is a greater chance that further revenue increases will start to flow through to the bottom line. The increase in margins should come as the Europe business grows, currently EBITDA margins in their Europe business are 18% against Australia at 32%. Australia is a mature business, whilst Europe has a greater runway for growth and hence the company is investing more there to grow the business.”

When we look at this year, we saw revenue continue to grow (+17%), and increasing operational leverage with EBITDA up 57% and NPAT up 74%. Europe was a big part of this with revenue rising 20% which outpaced growth in Australia.

Source: Company filings, author’s calculations

They also provided strong guidance with 15-20% revenue growth and increasing margins both expected. The position grew over the course of the year to be our largest, and we maintain it as that into 2026.

The other two stocks above (SRG Global and Mayfield Group) are both contractors, albeit in different industries. SRG Global is largely exposed to infrastructure construction and maintenance, whilst Mayfield is exposed to electrification and the rollout of data centres (and hence the AI trade). Whilst in different industries, the financials have been similar with increasing order books leading to higher cashflow, leading to higher dividends and acquisitions. We can also throw in Symal Group that we mentioned above as they operate in the same field as SRG and have seen similar drivers.

SRG have been regular acquirers since Covid, however their most significant acquisitions have come in the last 18 months. Firstly, in August 2024, they announced the acquisition of Diona. We wrote about that here:

It is fair to say we were positive on the acquisition at the time, writing:

“The strategic rationale makes a lot of sense, it diversifies the company further away from industries such as mining and construction into less cyclical industries, whilst also increasing the East Coast presence… It is rare that an acquisition ticks the boxes on almost every front, increasing the quality of the business, reducing the cyclicality and being earnings accretive. All of that and we still haven’t mentioned that it increases the Work in Hand by 50%.”

The signs through the first year of ownership have vindicated that positivity.

Then a few months ago, they announced another acquisition, this time of Total AMS Pty Ltd, known as TAMS. This time, the attractiveness was based on valuation. We covered this acquisition in our October update:

On the valuation, we wrote the following:

“The acquisition will cost the company $85m upfront, made up of a combination of existing cash and debt as well as shares issued to the vendors. A majority of the senior management are staying on and taking at least some shares, one founder is stepping aside and cashing out. There is also a two year earn-out program based on the EBITDA level. In return for these payments, the company expects TAMS to earn $200m of revenue and $35m of EBITDA for FY26. If the acquisition performs as expected, then the underlying multiple will be 2.7x EBITDA.”

Whilst SRG has undertaken a pair of significant acquisitions, Symal has taken a different approach and as mentioned above, made four small bolt-on acquisitions in a short period of time. Both approaches have been rewarded by the market at this stage of the cycle.

Mayfield is a little bit behind with regards to acquisitions. It’s growth to date has been organic; however, they did make a small acquisition recently paying $7m for BE Switchcraft. Following this, the company decided (a decision that was potentially aided by some brokers) to raise equity for further acquisitions. No further acquisitions have been announced yet, but the result of the equity raising has been increased institutional ownership and significant share price momentum. We do have concerns around the valuation, which we wrote about last month:

Since then, the share price has continued to rally, up 19.2% in December. As a result, we have taken some further profits.

One thing we do need to be conscious of is our overall weighting to contractors given their cyclicality, we have taken profits at various times in both SRG and Mayfield, but our weighting across the three above names still sits at 27.7%. Whilst momentum is strong, we look good, but we want to ensure that we don’t give too much back on the way down.

Just a friendly reminder that none of the above is investment advice, it is factual commentary on a portfolio run by the author.

Great update and fantastic emerging track record. Keep it up Guy!