I’m a little late with this post, and I have seen on twitter a number of people posting solid results for 2023. Adding to those, our portfolio returned 44.8% against the All Ords Accumulation at 13.0%.

Investing became easy in the last quarter as inflation expectations dropped and brought interest rates down with them. Lower interest rates, with all else being equal, push up asset prices.

Our return for year was largely driven by three companies.

MHM Automation (NZX:MHM), +78.5% for the year.

Gentrack Group, +144% (NZX:GTK) since our purchase in March.

Austco Healthcare (ASX:AHC), +66.7% for the year.

MHM had the biggest impact on the performance of our portfolio, as it was our largest position. We accumulated the position with purchases between March 2022 and July 2023. The green circles below represent purchases and the red circle represent the one sale we have made to date.

Source: Yahoo Finance

As you can see and you would know as a regular reader, the performance of the portfolio had a significant boost in early November when MHM received a takeover offer at $1.70 per share, representing a 132% premium to our average purchase price.

Acquisitions are always a nice bonus when you get them, they often come from nowhere. MHM was a rollup story, and the early drivers of the returns we saw were from the acquisition of Wyma just over a year ago. We wrote about that acquisition here:

As you can see and you would know as a regular reader, the performance of the portfolio had a significant boost in early November when MHM received a takeover offer at $1.70 per share, representing a 132% premium to our average purchase price.

Acquisitions are always a nice bonus when you get them, they often come from nowhere. MHM was a rollup story, and the early drivers of the returns we saw were from the acquisition of Wyma just over a year ago. We wrote about that acquisition here:

2023: Writing More

I setup this blog a few years ago with the idea of writing regularly. Unfortunately, life, as it often does, got in the way. Over the last four years, I have moved country, started a new job focused more on the Macro side of investing and have bought a house. This combined with what I considered irrational markets meant that overall, I had little time t…

We were expecting more news flow like that. However, the acquisition of Wyma led to the company doing more business in the US and eventually led to them selling themselves to a company over there. The price offered, in our opinion, was generous and as a result, we were happy to take the money.

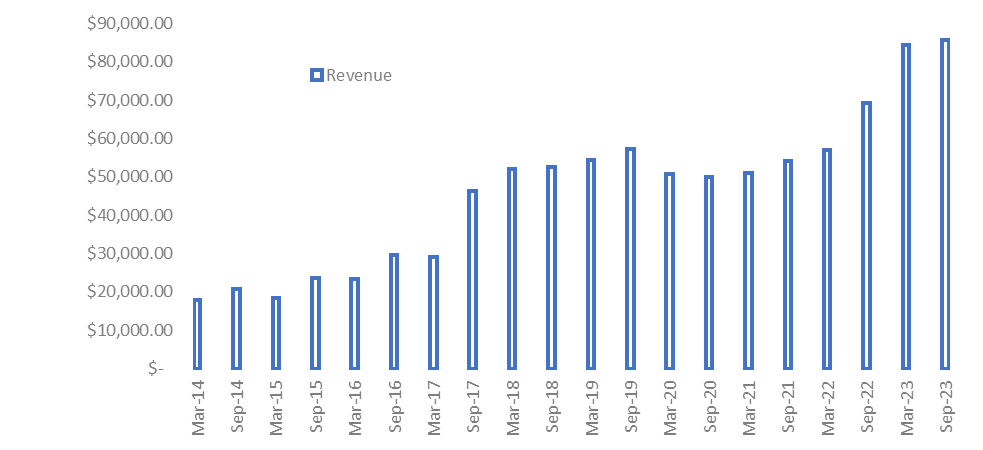

Gentrack is a different story. It is a company we have owned in the past and made good money on. Following a disastrous acquisition in the UK, the company had to endure years of pain due to customers facing bankruptcy. A refresh of management, some cost cutting, and a new strategy has seen the company come through the worst and return to growth. This is seen via revenue at this stage, and the expectations are for strong growth earnings over the next few years.

Source: Company Filings

The shares have had a very strong run on the turnaround and the company needs to deliver to justify the recent rally.

Finally, Austco Healthcare shares have had a strong year, which we have benefited from. However, it is probably a bit early to say we are right on this one. An increased sales team in the US has seen some semblance of revenue growth.

Source: Company Filings

In addition, the open sales orders book has grown to a record $40.7m with the company regularly announcing decent contract wins over the course of the last year. The only thing lacking is profit and we expect to see that come through in FY24. The upfront cost of building out the sales team has meant profit growth has lagged revenue growth, this hopefully will change.

One other positive is the recent settlement of the Teknocorp acquisition, which in effect adds to their Australian sales team as it operates currently as a supplier of their equipment to hospitals. Teknocorp also adds $1.25m to the company’s EBTIDA line, hopefully helping that profit growth.

The final thing we hope to see this year is the continuation of the growth in Software revenue. Software revenues grew 65% to $8.5m and if the current trajectory continues, it could become a meaningful component of the earnings. The software component is particularly attractive given its incremental margins are significantly higher than the hardware piece.

Those were our successes for the year, however in investing, you never get everything right. Thankfully, this year our mistakes did not cost us a significant amount. The two positions we sold that we lost money on were:

Vitura Health (ASX:VIT); and

SDI Limited (ASX:SDI).

Vitura Health was in our opinion the more embarrassing mistake of the two. It was embarrassing because we identified the key risk upfront. This risk was management and the fighting of two groups for control of the company. Thankfully, due to identifying that risk we kept the position small, and when the existing management team made an acquisition well outside of the company’s core competencies, we reacted quickly by selling. In doing so, we limited our loss on the position to 3.1%. With an average selling price of just under 36 cps, it could have been a lot worse. The shares finished the year at 25.5 cps and now face challenges around a software provider to their key asset, the Canview platform.

SDI was also a small position. It is a company that we have followed for some time and owned in the past. Recent results showed decent growth out of the pandemic, and we were intrigued the company’s plan to boost production via its planned new facility (although we still believe they need a capital raising to fund it). During the first four months of the financial year, sales fell, and expenses were up. As a result, we felt the near-term valuations were stretched, and that combined with the added unknown of when and how they will raise capital, we thought the uncertainty outweighed the potential upside. Unfortunately, we jumped the gun here and the company had a very strong last 2 months of the year on the back of two new product releases. We sold out at a loss at 10.3%. Despite the positive news since our sale, the shares remain around the level we sold at, meaning we could buy back in if we wished to. At this stage, we will remain on the sidelines until we receive more clarity around their new site and the funding associated with it.

We do currently have some buying power and are actively looking at a few new ideas. Given the rally over the last few months, nothing is standing out currently, but we continue to try and find new places to allocate capital.

Just a friendly reminder that none of the above is investment advice, it is factual commentary on a portfolio run by the author.