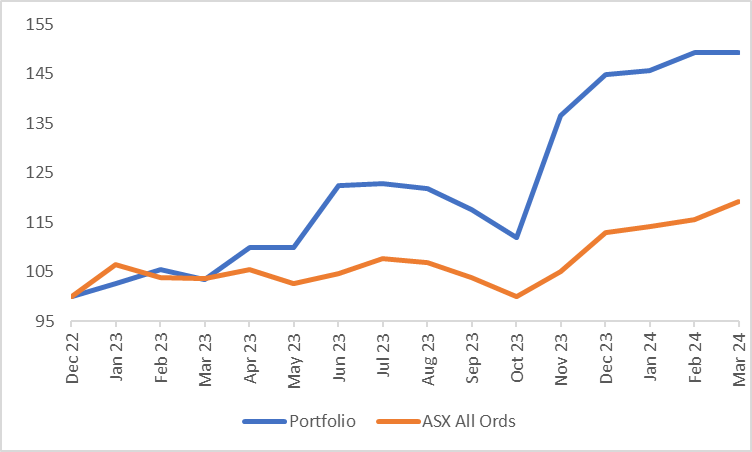

Our portfolio fell 0.03% in March against a market that rose 3.11%. Since inception our portfolio is up 49.3% against the All Ords Accumulation up 19.1%.

The main drag on the portfolio was Close the Loop Group (ASX:CLG) which fell 21.3% in March. We bought some more Close the Loop and it is now our largest position, as stated last month we were surprised with the market reaction to the result, and for now we remain “Long and Wrong”. Helping offset this fall were gains in our next two largest positions, Gentrack Group (NZX:GTK) up 11.9%, and SRG Global (ASX:SRG) up 5.8%.

The rise in Gentrack continues to surprise us, we are now up 228% on our purchase just over a year ago.

Source: Google

We wrote about Gentrack’s last result back in November.

At the time, we extrapolated the company’s guidance and came to a FY27 EBITDA of $45m. After the recent rally, the market cap is now $918m and the Enterprise Value is $881m (taking into account the $12m investment in Amber Energy), placing it on FY27 EV/EBITDA multiple of 19.6x and a FY27 P/E of somewhere close to 30x. This is three years away, so it is fair to say that a lot of the projected earnings growth has been factored into the share price. We haven’t sold any yet, but it is getting tempting to trim the position. Tech stocks have driven the market through the first quarter of the year as seen by the leading performers in the ASX 200 and S&P500. We have been more focused on the value side of the market in recent times, but having the exposure to Gentrack has meant we haven’t completely missed out on the growth rally.

The top performers in the ASX200 have been:

Source: Bloomberg

Whilst in the S&P500:

Source: Bloomberg

We haven’t sold any Gentrack yet, but we have made a few adjustments in the portfolio following reporting season. One of the major changes was to completely exit Austco Healthcare.

The key concern we have with Austco is earnings quality. We are seeing revenue growth and expect that to continue. The company had guided to an increased expense base and hence profit has fallen. Now the guidance is that the expense growth will moderate and profit will grow. That sounds positive, and with a few recent acquisitions, earnings could be materially higher in the near term. Of course, they need to be higher with the shares currently trading on 27.5x the last 12 months profit.

The concern we have is not the valuation or the earnings growth, it is the cashflow. The below chart compares Net Profit after Tax to Free Cash Flow and since Covid, there has been a major disconnect.

Source: Company Filings, author’s calculations

Over the last 12 months, the accounting profit has been just over $2m whilst the Free Cash Flow has been -$814k. The cause of the disconnect is the capitalisation of software development. One of the key goals of the company is to expand its software offering and hence, their software revenue. In order to do this, they have to invest in research and development. In putting that R&D through the balance sheet, they are potentially overstating their profit.

All of this is fine, if they get a return on the cash they are spending, so we need to look at the software revenues. Last half, the software revenues were up $0.4m on the prior corresponding period, however they capitalised more than double that on R&D.

Source: Company Filings

However, the chart above from the company is a little misleading. Half on half, software revenues actually fell.

Source: Company Filings

Overall, the growth in software revenue should increase with the hardware sales. This half may be a short-term blip, but there is little to backup the balance sheet investment at this stage.

The lack of Free Cash Flow combined with recent acquisitions has meant the company has started to burn through its cash pile.

Source: Company Filings, author’s calculations

When we bought into Austco Healthcare, it was a company sitting on a large cash pile relative to its market cap, trading on a low multiple and with growth prospects. From that list, only really the growth prospects remain, with only 6% of the market cap in cash and the company trading on 27.5x the last 12 months earnings.

We took the proceeds of the Austco sale and increased some of our existing positions. The three we added to were:

Scott Technology (NZX:SCT);

Close the Loop (ASX:CLG); and

EVZ Limited (ASX:EVZ).

We will look at Scott Technology and Close the Loop here.

Scott Technology

Scott Technology shares fell 9.1% over the month and are down 18.6% year to date. The reason for the fall this month was the exit of the CEO and CFO within 4 days. The CEO had been there for 4 and a half years, he was brought to turnaround the business and has done a great job. The CFO was leaving for the same role at a larger company (Tourism Holdings). In light of the CFO departure, the CEO has agreed to delay his departure from the firm.

Normally, the departure of the top two executives of the firm would be a major concern, however both had their reasons. In addition, the company put out a trading update with the first half set to see double digit growth in revenue and EBITDA. This continues the positive trends we have seen lately.

Source: Company filings

NPAT growth will likely be lower due to IFRS16 standards. The company has moved into larger facilities in the Czech Republic and their Rocklabs division has done likewise in Auckland. As a result of larger facilities, depreciation on “right to lease” assets will go up, but EBITDA is boosted as the rent expense is lower. Despite these technical issues, the key will be Free Cash Flow and based on the guidance, we expect a reversal of the last half this time around.

Source: Company filings, author’s calculations

From the AGM back in November, we know that core business units are all performing well. Rocklabs is riding the mining cycle and Bladestop sales have been growing everywhere. The manufacturing division has been a bit more volatile, but the new facilities in Europe indicate that the company believes in their growth trajectory.

After the fall, the company now trades at 14.5x last years earnings. Last year, the company undertook a strategic review which seemed aimed at selling themselves, however it was unsuccessful. We still believe the best path forward is a breakup, and believe the three core divisions could be spun out to willing buyers. However, the sale of the business is off the table for now. We are still comfortable with the products the company is selling, the momentum of the business and the valuation of the shares.

Close the Loop

We have continued to buy Close the Loop and we continue to be wrong. One of the areas of concern from the recent result was the decline in the packaging division. When the company listed, that was the core business. The acquisition of ISP Tek Services has changed that.

Source: Company Filings

Packaging revenue fell 14% from the prior corresponding period, whilst resource recovery revenue rose 231%. Most of that growth is from acquisition as it is the first full half contribution from ISP Tek Services. In order to get an approximation of the organic growth, we can take the ISP runrate revenue prior to acquisition (US$24.5m or c. A$37.7m) and add it to the existing Close the Loop recovery revenue from the pcp. This gives us a base of $59.2m and suggests that organic growth is around the 20% mark.

So, we have the larger division (Resource Recovery at 69% of the 1st Half revenue) growing at 20%, whilst the smaller division is falling 14%. Overall, the company is growing but there is clear concern from the market about the original listed business. We bought in after the ISP acquisition, we believe that to be the more attractive business and that is where the growth is coming from.

At a share price of 29.5c, the company trades at 5.8x NPATA and 8.5x Free Cash Flow (note we have doubled the first half for these estimates as that is the first result with a full six months of ISP Tek Services).

Just a friendly reminder that none of the above is investment advice, it is factual commentary on a portfolio run by the author.