Please note this post is too long for some email providers, please click through if you wish to see it in its entirety.

November was a strong month; the portfolio was up 21.9% against the All Ords Accumulation up 5.2%. Year to date, the portfolio is up 36.6% versus the market at 5.2%.

The performance was largely driven by the takeover bid for MHM Automation (NZX:MHM), the shares soared 80% and that alone added just over 16% to the portfolio performance. The other significant contributor was Gentrack Group (+18.4%), who reported their annual results which showed the business turnaround continues. We added one new position and sold out of one existing position over the course of the month, which we will touch on below.

Gentrack Group (GTK:NZX and GTK:ASX)

As mentioned, Gentrack reported their annual result during the month. The market reacted positively to the results, as the outlook shows the impact of the declining UK business disappearing and the company outside of that growing strongly. Meaning that the turnaround in the business sees it coming out the other side.

For those interested in the history of how Gentrack got themselves into trouble via acquisition in the UK, at a time when regulation was changing, we wrote about it extensively back in 2021:

At that time, we didn’t take a position, but we did add it to our watch list. We ended up entering a position in March this year, which we wrote about here:

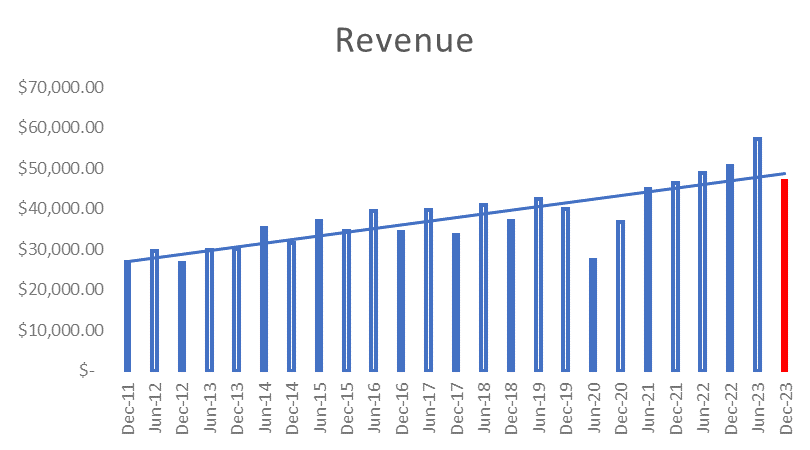

We are currently up 128% on that purchase. So, what has led to the rally? Firstly, the company has returned to revenue growth. The first half this year saw a significant increase and the full year year-on-year numbers look very strong. The increase was 36.7% over the last 12 months but when we strip out the impact of UK insolvencies, the growth was 47%.

Source: Company filings, author’s calculations

Next year, the company is set to lose a further $27.6m of revenue from the UK due to insolvencies. Despite this, they have guided to revenue “being at least in line with FY23.” This implies organic growth on the remaining business of at least 16%. On this front, the company has announced a first contract win in Saudi Arabia, and a big upgrade at Genesis Energy in NZ. Two decent contracts which underpin some of this growth.

EBITDA is expected to be largely flat as well, with the new contracts won there is some upfront investment that is expensed, as a result margins should rise over time as the business grows and that investment becomes a smaller percentage of revenue. Thankfully, Gentrack has in recent years returned to an accounting standard of expensing all R&D which makes their financial statements very clean.

The company has maintained their medium-term targets, after upgrading FY24.

Source: Company Filings

Taking the 15% growth rate over the three years, revenue would grow to $258m. The midpoint of the EBITDA margin, would therefore give EBITDA of $45m. The current market cap is $638m and the company is sitting on $49m of cash, giving an EV of $589m. This in turn gives a FY27 EV/EBITDA of 13x. So, looking out a few years, we can start to justify the current valuation, noting that on current numbers, the shares look very expensive.

One thing worth focusing on is that cash pile. The company has elected not to pay a dividend and appears to be eyeing the possibility of an acquisition. Given the company’s history and in particular the acquisition of Junifer Systems back in March 2017, some may be nervous about this development. However, this is a new management team and they appear to have the company back on track. They have been doing the right things from a turnaround and an organic growth perspective, so they probably deserve a chance to take this business further via acquisition, the market through the share price rise is telling us that they definitely do.

SDI Limited (ASX:SDI)

We mentioned above that we exited one position during that month. That position was SDI Limited. We wrote about their recent result back in our August update:

At the time we noted that the result was mixed, with revenue up but profit down. Part of the reason for the fall in profit was an increase in travel and marketing costs. That marketing had appeared to show some positive impact in the 2nd half of the last financial year with strong revenue growth, however at the AGM in November, the company put out the following update.

Source: Company Filings

If we extrapolate those trends for the remainder of the first half, we get an ugly picture for revenue.

Source: Company filings, author’s calculations

With increased costs and decreased revenue, the EBITDA exploration is even worse.

Source: Company filings, author’s calculations

Historically, the shares trade on a P/E in the low double digits. Currently, they are on a 13x historic multiple with the prospect of declining earnings. Couple in the fact that they will most likely need to raise capital sometime in the future to fund their new facility, and we have the feeling we will be able to buy the shares back at a cheaper price at a later date. Also, you have to question the sustainability of a larger manufacturing base if they are struggling to consistently grow sales currently.

We sold out but will maintain a watch on the company, believing there may be a future opportunity here. It was our smallest position, and we viewing the new facility as having some option value but that only works if they can continue to grow.

Finally, the position we purchased this month was Environmental Group (ASX:EGL). We wrote some brief thoughts on that position here:

We won’t add more on the company here but do from a philosophical side want to add some thoughts. In investing, there are a lot of different ways to do things. From a value perspective, you can buy companies at a cheap multiple and hope for a rerate. Our positions in SRG Global and Close the Loop are in that vein. The position in Environmental Group is different in that looking at the metrics, it is not obviously cheap but the turnaround from the new management team gives us some confidence that in the next few years these numbers will look very different. This is similar to the situation with MHM Automation, where we bought a company that hadn’t been profitable moving into profitability. The risk in these positions is that the turnaround doesn’t materialise, however the upside is significant if it pays off. We have seen that with MHM and more recently Gentrack which has switched from a turnaround to a growth stock. Initially, in these positions we start with a small amount and look to grow it over time as the story plays out.

Ultimately, we don’t want to be pigeonholed as investors, and are open to ideas that would be defined as value or growth. At the end of the day, everyone is just trying to buy something at a lower price than the discounted sum of the future cashflows and that is what we are focused on.

Just a friendly reminder that none of the above is investment advice, it is factual commentary on a portfolio run by the author.